Agent / Broker Merger & Acquisition Summary

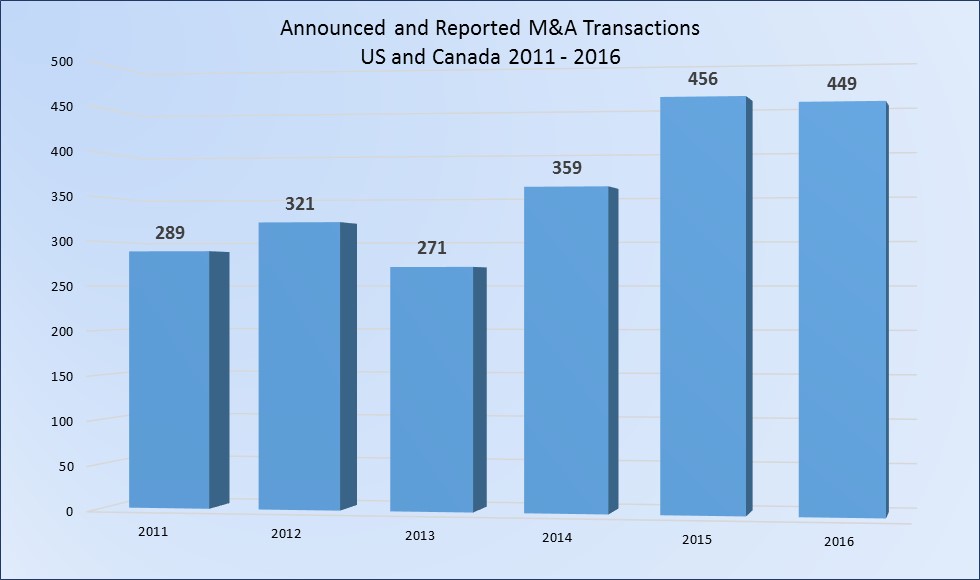

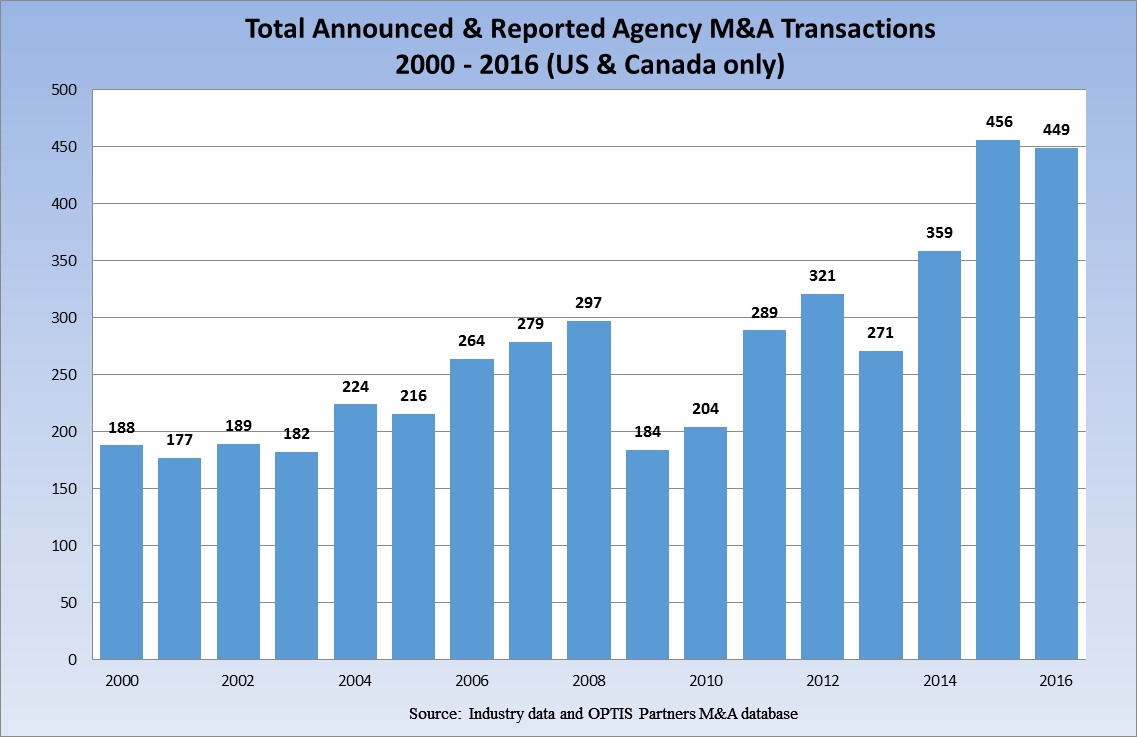

M&A Activity during 2016 fell just short of the 2015 count, with reported transactions in the US and Canada down slightly from 456 in 2015 to 449 in 2016, but still the second highest level of M&A activity on record.

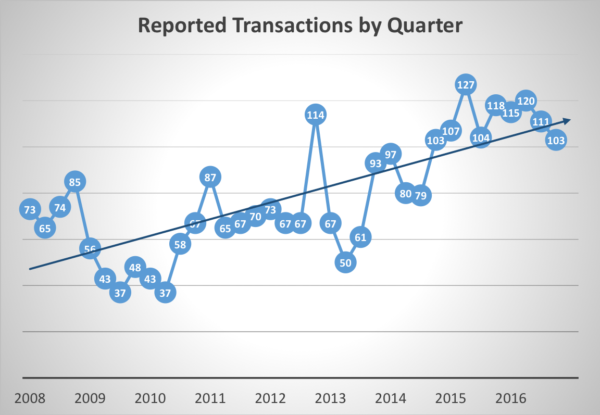

Reported Transactions by Quarter

Breaking the data down into quarterly activity levels, we’ve now had nine quarters in a row with greater than 100 transactions.

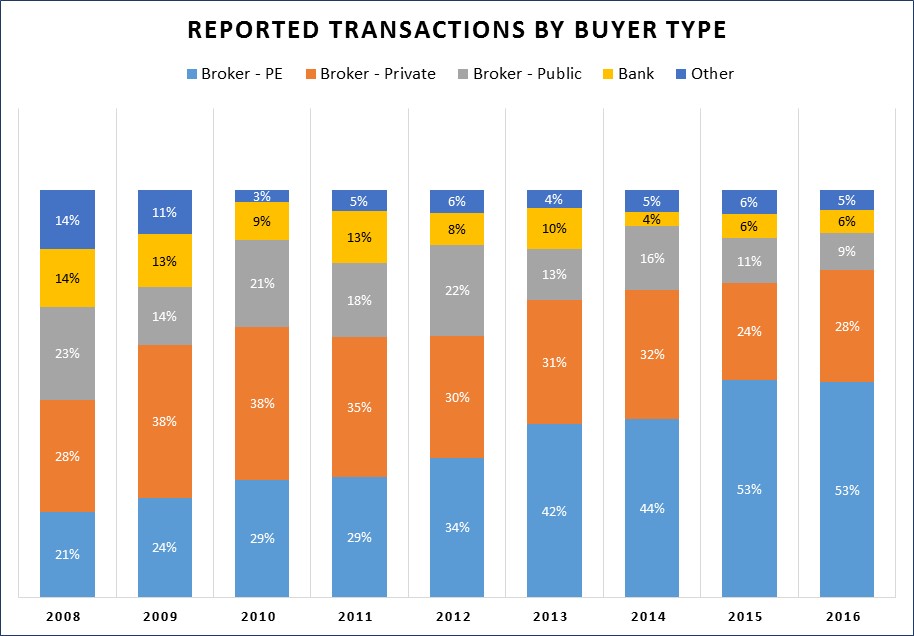

Reported Transactions by Buyer Type

Private-equity backed firms (“PE-backed”) continue to dominate the buyer landscape, holding steady at 53% of the total transactions in 2016, up from only 21% in 2008 while most of the other buyer categories have shown declines over the same period:

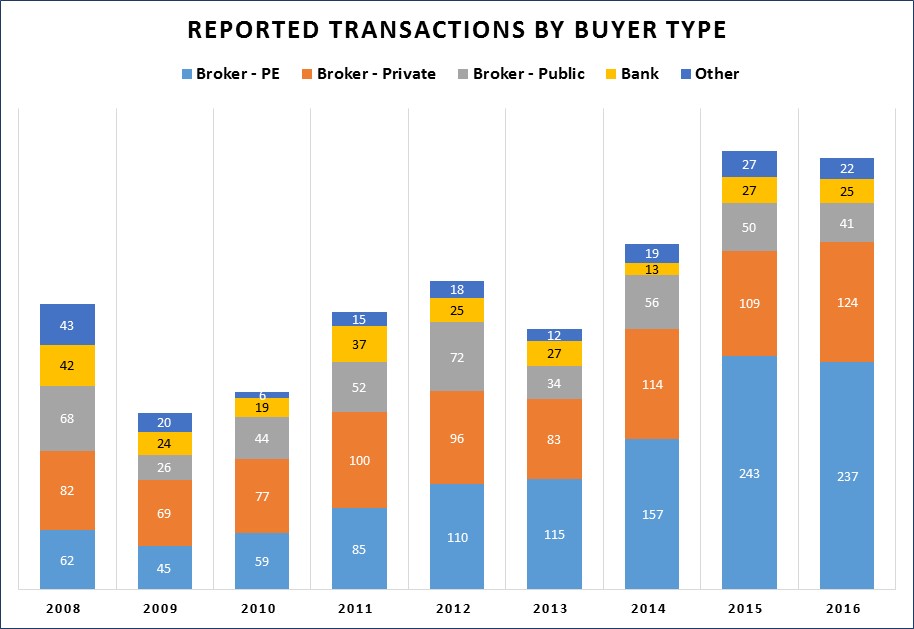

Another way to look at the activity by type of buyer is the actual number of transactions, with virtually all of the growth in the total count coming from increased activities by the PE-backed buyers and the privately owned buyers:

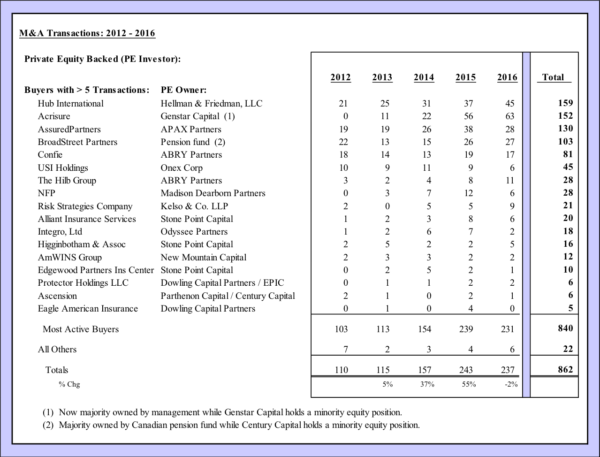

Buyer Group Activity Over Time

The table below illustrates the activity levels of the different buyer groups over time, comparing the average number of transactions per year over the period 2008 through 2016:

Although the number of buyers in each category has moved around, the two most active groups in terms of average deals per buyer have had a relatively stable number of participants over the past 8 years. However, the number of deals and the average number per buyer has changed dramatically for these two groups. The PE-backed buyer group has increased from less than 4 transactions each to an average of about 12.5 deals while the publicly traded brokers has dropped from an average of 9.7 deals each to less than 7. For the others, although the number of transactions has increased for the privately owned and decreased for the others, this is such a disparate group with few firms completing more than one or two deals each year.

Key Transactions

Included in the results shown above were several transactions in 2016 with some of the largest agencies, including the following:

- Feb, 2016, BB&T (bank) purchased Swett & Crawford, the North American operations of CGSC North America

- Apr, 2016, Broadstreet Partners (backed by the Ontario Teachers’ Pension fund and Century Capital) purchased Sterling & Sterling, #61 on the Business Insurance Top 100 in 2016

- Jun, 2016, Prime Risk Partners (backed by Thomas H. Lee Partners) purchased Old National Insurance, #101 on the Business Insurance Top 100 in 2016

- Jul, 2016, Alliant (backed by Stone Point Capital) purchased Mesirow Insurance Services, #41 on the Business Insurance Top 100 in 2016

Not included in the numbers above are three transactions during 2016 where the private-equity firm sold their interest in an existing agency or new private-equity money entered the marketplace:

- Jun, 2016, Connor Strong & Buckelew sold a minority interest in their firm to Century Equity Partners

- Oct, 2016, New Mountain Capital sold their position with AmWINS Group to Dragoneer Investment Group

- Oct, 2016 Genstar Capital sold the majority of their interest in Acrisure to a management-led buyout of the firm

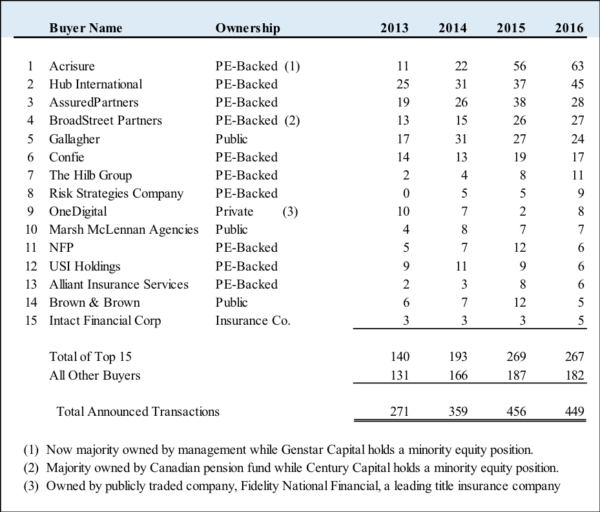

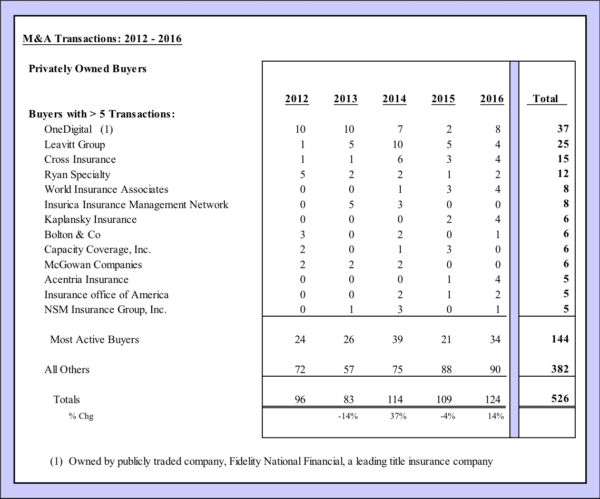

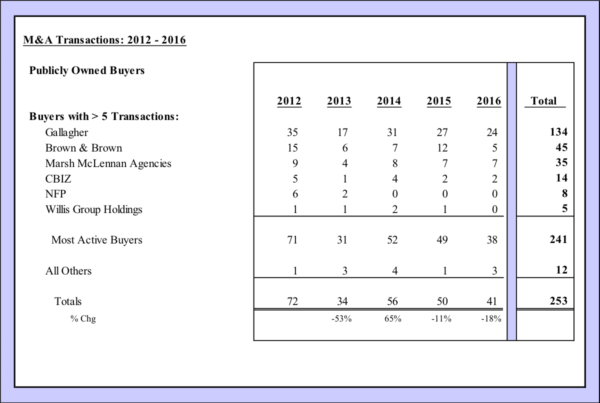

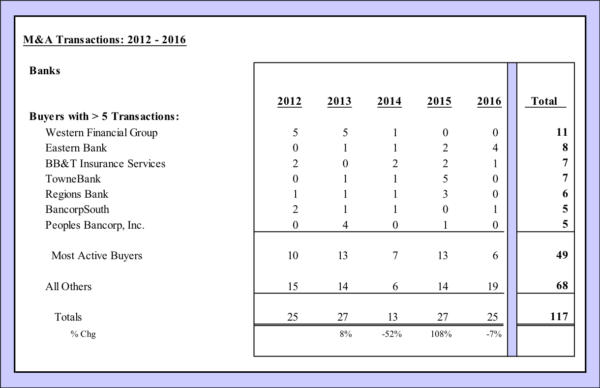

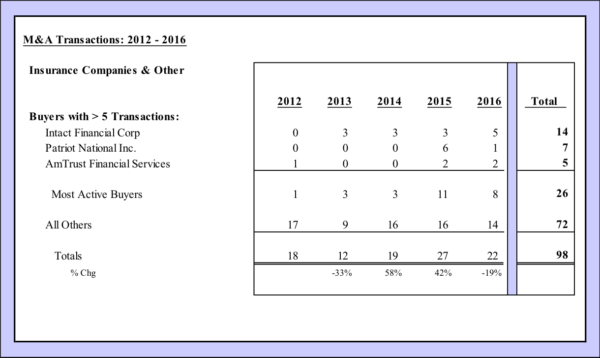

Individual Buyer Activity

Looking at the individual buyer activity, we know not all transactions from all buyers are reported, with some of the larger buyer firms only reporting transactions of a certain size whereas other buyers include all acquisitions regardless of size. Based on the reported transactions, the most active buyers in 2016 are shown in the table below, with comparison totals for the last couple years:

Over the past two years, Acrisure has completed over 13% of all announced transactions, closing more than 1 deal each week and nearly 50% ahead of their next most active buyer. Although Acrisure recently completed a management buy-out of a significant portion of their private-equity backer, we believe they will continue to behave much like other PE-backed firms with their 3rd-party debt-capital partners

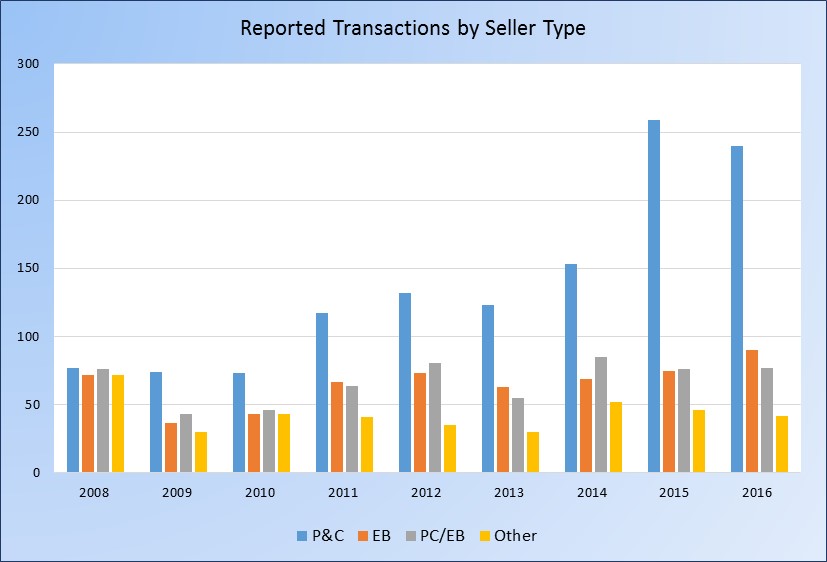

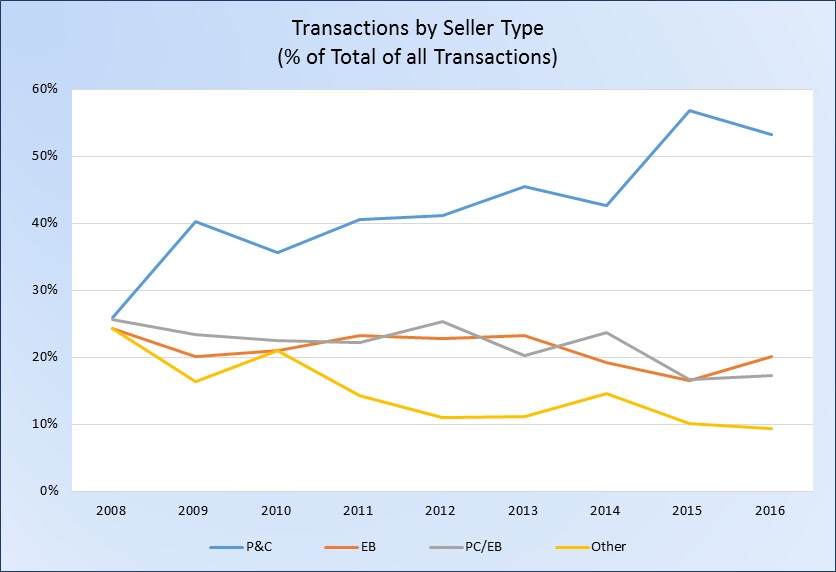

Reported Transactions by Seller Type

The distribution of transactions between the different types of sellers are illustrated in the following two tables, the first showing the actual number of transactions and the second showing the percentage allocation between the four categories:

The growth in P&C firm sales jumped dramatically in 2015, but dropped off slightly in 2016 while the other seller groups remained relatively stable, albeit a slight increase in the number of Benefits agency sales.

The combination of the slight pull-back in P&C transactions and the increase in Benefit agency sales in 2016 caused some minor changes in the distribution of transactions.

Summary:

The agency M&A world remains very active, with aggressive buyers and plenty of sellers. Interest rates remain low but starting to slowly move upward, and money is readily available for investing in the insurance broker community. Our closing comments remain similar to what we have said in the past:

- Valuation pricing is driven by the underlying value of the business and by market competitive forces, both of which have many contributing factors. In many ways, what we have been experiencing over the past couple years is a “perfect storm” for the benefit of sellers. Like all storms, they eventually pass and calm returns.

- Buyers, in particular the smaller and less capitalized firms, need to be careful not to get carried away in the pricing competition for a seller’s business only to find out later they can’t afford to pay for it.

- Firms wrestling with trying to perpetuate need to be steadfast in their realistic valuations for internal transactions without getting overly swayed by actual and anecdotal pricing stories of other agency transactions. Remember, in a perpetuation process, there are no buyer synergies or strategic value that the buyer can utilize to enhance the value of the transaction.

- For agency owners waiting for the “right time to sell” before jumping on the bandwagon, be careful not to let the last one pass you by. This remains a sellers’ market likely for the near term future, but it won’t last forever.

- Finally, if you’re neither buyer nor seller, ignore all the hype and stories about how much others have sold for and focus instead on finding the right people to help you grow your agency and improve your metrics every day. Keep your long-term plans in sight and take the necessary steps to position yourself to achieve your goals.

Appendix A

Appendix B

Appendix C

Appendix D

Appendix E

Appendix F

Explanation and sources of data:

Data is for U.S. and Canadian transactions in the insurance distribution sector for both retail and wholesale producers, including managing general agencies/managing general underwriters (MGA/MGU). These agencies and brokers provide property/casualty insurance, employee benefits, or any combination thereof.

Firms with private equity backing are identified in the chart on p. 8 and Appendix A on p. 12

Data for reported and announced transactions have been obtained from various sources, including press releases, trade press articles, company websites and direct communications with buyers.